Financial security is a fundamental need of many people. Just as Life insurance policies are often taken out to ensure that family members and others are well cared for in the event of death, what happens if one gets seriously ill or suffers a serious accident? In those cases, the financial needs of the family may be particularly high.

Critical Illness1 (CI) and Disability insurance products are available to remedy this situation. Although these are generally very useful for insured persons, such insurance plays a minor role in many insurance markets compared to pure Life insurance.

The design options and potential of these insurance products are perhaps not sufficiently known or appreciated globally.

This blog looks at the various ways in which these products can be designed. The most diverse needs of potential policyholders can be covered and, at the same time, insurers can have the opportunity to offer affordable insurance premiums.

CI insurance – a concept with many possibilities

CI insurance is characterised by a lump sum benefit payment upon diagnosis or the occurrence of a predefined illness or injury. In many markets, CI insurance policies exist with a variety of defined conditions, each of which can trigger a claim. In practice, cancer, myocardial infarction (heart attack) and stroke are by far the most common cause of an insured event.

We see that in CI products with many different benefit triggers, these three diseases often account for 80%–90% of claims, with cancer accounting for about 80% of claims in women.2,3 Cancer is also the most common cause of claims for men, but heart attacks and strokes are far more significant in this group, accounting for about 30% of claims in total.

In principle, a distinction must be made between two different concepts. First, there is the so‑called “accelerated CI benefit” that pays out all or part of the death benefit prematurely if a serious illness is diagnosed. On the other hand, there is the “standalone CI benefit” that can be taken out with or without life insurance. This is characterised by the benefit amount being often paid out only once the insured persons have survived for a certain period after the insured event.

The principle of CI insurance can be adapted to the needs of the customers in a variety of ways. The basic questions for structuring a CI insurance product are:

- Which conditions should the insurance cover?

- At what level of severity should benefits be paid?

In addition, it is possible to make the benefit amount dependent on the severity of the illness. For example, only a portion of the CI cover can be paid out if cancer is diagnosed at an early stage. If the cancer progresses, the remainder of the sum insured could be paid to the insured persons.

Moreover, CI insurance can be designed in such a way that it does not terminate when a serious illness is diagnosed, so that it provides financial protection for one or more other diagnoses during the insurance term. This may be of particular interest to the insured persons, as they usually have poor chances of taking out a new CI insurance policy or a similar insurance product after a serious illness.

Disability insurance – deferred period and degree of disability are key parameters

Disability insurance must be differentiated from CI insurance. The purpose of Disability insurance is less to cover the illness or injury of the insured persons per se, but rather to cushion the financial losses resulting from an accident or illness-related inability to work. For this reason, disability benefits are often monthly payments.

Disability insurance can be designed in different ways. For example, the insurance may be structured in such a way that a payment is made only when the duration of the inability to work exceeds a certain period (the deferred or deferment period; in some markets called the waiting or elimination period). With regard to incidence rates and the associated premium calculation, there are various levers that can be used when designing Disability insurance.

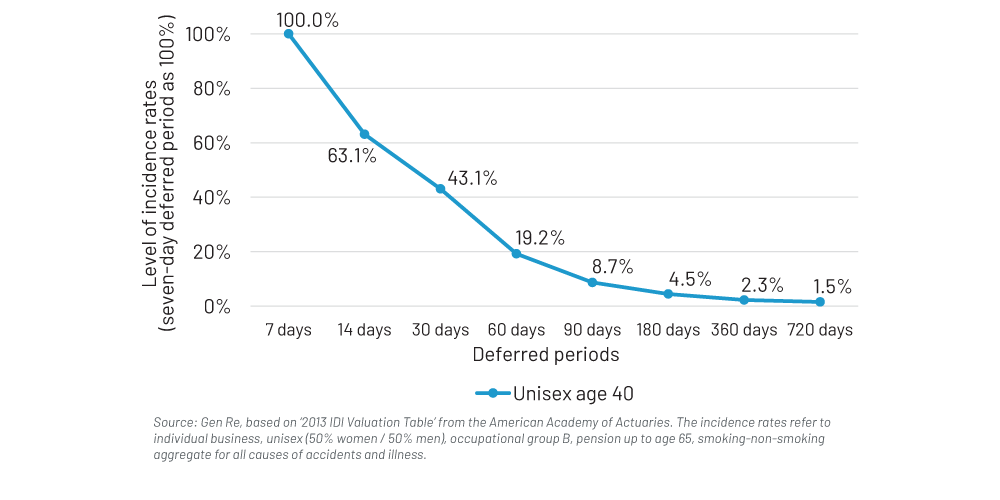

For example, the length of the deferred period has a significant influence on the probability of occurrence and thus on the amount of the premium. The chart below, based on US data, shows how deferred periods impact incidence rates as a percentage of a seven-day deferred period. Based on these data, the probability of occurrence in 40‑year-olds (50:50 men:women) decreases to 63% if the deferred period is increased from seven to 14 days.

This level decreases continuously with longer deferred periods, so that the deferred period is one of the most important factors in determining the amount of the insurance premium. In the case of Disability insurance with pension benefits, however, it should be noted that a change in the deferred period, and thus the probability of an insurance benefit, is not transferred one-to-one to the insurance premium, as short-term losses have a lower loss burden than long-term losses.

Influence of the Deferred Period on the Disability Incidence Rates in the US